Armenia: The Beginning of the End

Commentary by Nicat Hajizadeh, Department Head at CAERC

The most vivid indicator of Armenia’s “failed state” status is the severe imbalance of its balance of payments. Armenia has the most strained balance of payments in the South Caucasus. The balance of payments is a mirror of a country’s economy. Armenia’s macroeconomic and financial stability, including its monetary and exchange rate policy, is directly dependent on the condition of the Balance of Payments.

Long-standing political dictatorship and internal instability in the Republic of Armenia have created a syndrome of accumulated economic deficiencies. Under such an unfavorable business environment, the unattractiveness of capital investment by foreign investors (non-residents) is clearly reflected in Armenia’s balance of payments. The country’s geographically disadvantageous position, along with unfounded territorial claims against neighboring states, has excluded Armenia from logistics and transport corridors that drive foreign trade. In addition, the country’s mountainous terrain limits the production and export of agricultural crops and plant-based products.

In Armenia, economic, geographic, and political “inferiority complexes” form a complementary structure, creating threats not only at the national but also at the regional level. The occupying policy pursued by Armenia’s political leadership in connection with the Nagorno-Karabakh conflict has a negative impact on all parameters of the balance of payments, including foreign investment attractiveness.

The “Chronic Disease” of the Current Account

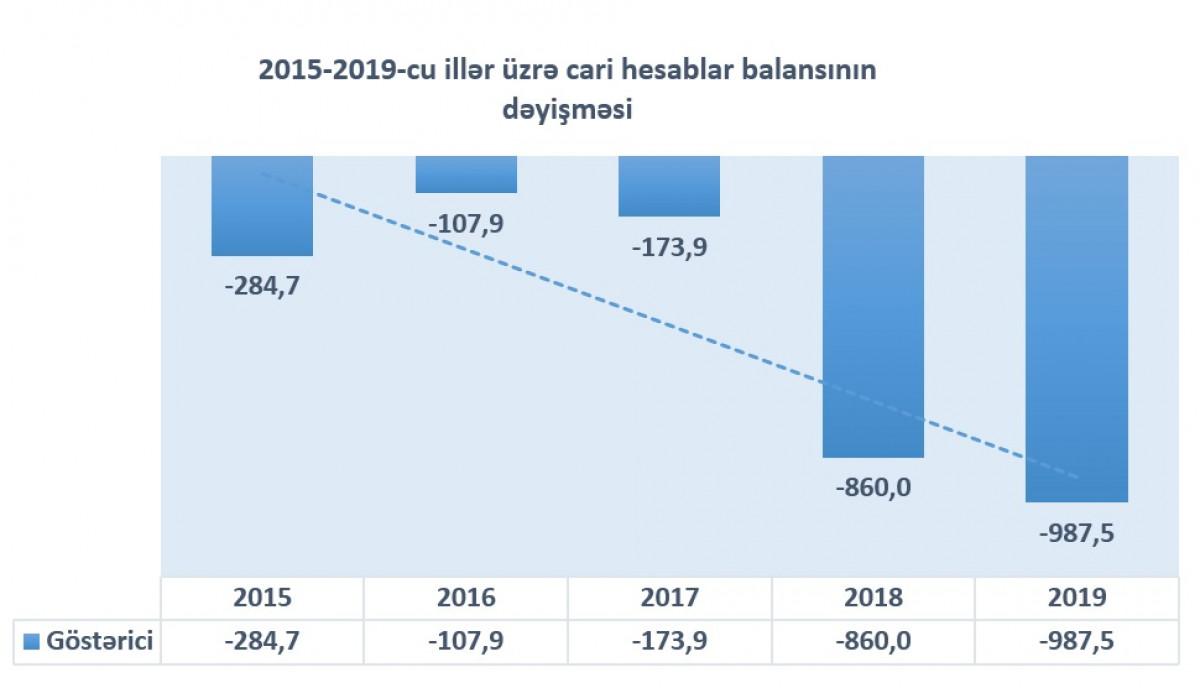

According to statistics published by the International Monetary Fund, the negative balance of the current account in 2019 amounted to USD 987.5 million.[1] In particular, a deficit of USD 1.8 billion was recorded in the structure of goods and services within the foreign trade balance, resulting in an overall deficit of USD 3.6 billion.[2] These figures, based on statistical data, indicate that Armenia entered the COVID-19 pandemic unprepared.

It is no coincidence that Armenia ranks among the “top 25” countries worldwide in terms of COVID-19 deaths per one million population and is the leading country in the post-Soviet space by this indicator. Due to the pandemic, Armenia’s emergency procurement of medical equipment and pharmaceuticals will directly contribute to a further widening of the current account deficit. Initial data from the Armenian Statistical Committee already show that orders for medical equipment and pharmaceuticals have moved to the top positions in the import structure. Moreover, the rapid increase in retail trade turnover in Armenia suggests that demand for these products will remain long-term.

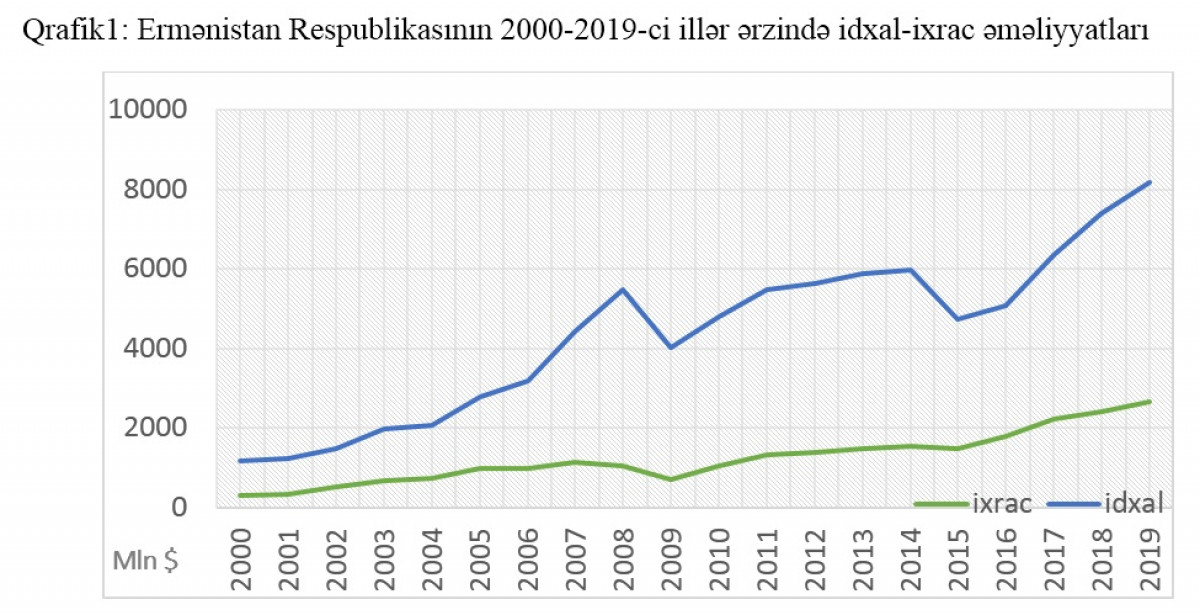

Based on the database of the Armenian Statistical Committee, the country has not recorded a positive foreign trade balance at any point since 1991. In line with the level of its economic potential, the negative balance over the past five years has been estimated at around USD 2–2.8 billion. According to data released by Armenia’s statistical authority, foreign trade turnover declined by 10.2 percent in January–August 2020. In addition, after trade turnover hit its lowest point in April 2020 with a 27.8 percent decline, the contraction began to slow. Nevertheless, a renewed sharp decline in exports started in July.

Ultimately, one of the main reasons for the instability and decline in exports is the heavy dependence of the vast majority of exported final products on raw material components, as well as the low level of commodity and geographical diversification of exports.

The level of export diversification in Armenia is low. According to export statistics for the first quarter of 2020, the main products dominating the commodity structure of exports include copper ores and concentrates, ferro-alloys, gold, jewelry and their parts (35.4%), food products, tobacco, alcoholic and non-alcoholic beverages (29.4%), and precious and non-precious stones, metals, and metal products (13.1%). Together, these three sectors account for nearly 80 percent of total exports. Since a significant share of the mining sector workforce consists of men, the mobilization declared in Armenia restricts production in the mining sector and reduces export revenues. Due to the COVID-19 pandemic, global prices for mineral raw materials have declined, which will reduce revenues from Armenia’s main export products. This is because the export deflator has entered negative territory as a result of lower global market prices.

One of the key barriers to Armenia’s exports is the remoteness of export markets and limited transport and logistics capabilities. This year, due to COVID-19, exports of tourism services have also fallen to a minimal level.

Starting this year, Armenia will no longer be able to re-export vehicles to Kazakhstan, which will further reduce export revenues. As a result of non-tariff regulations imposed by Kazakhstan on automobile imports from Armenia, demand for these products has declined, and the incomes of Armenian entrepreneurs have fallen. In 2019, the number of vehicles re-exported via Armenia tripled, reaching 189,000 units. Trade restrictions applied to automobiles, as well as to other products, will negatively affect Armenia’s exports.

The Weak Link of the South Caucasus

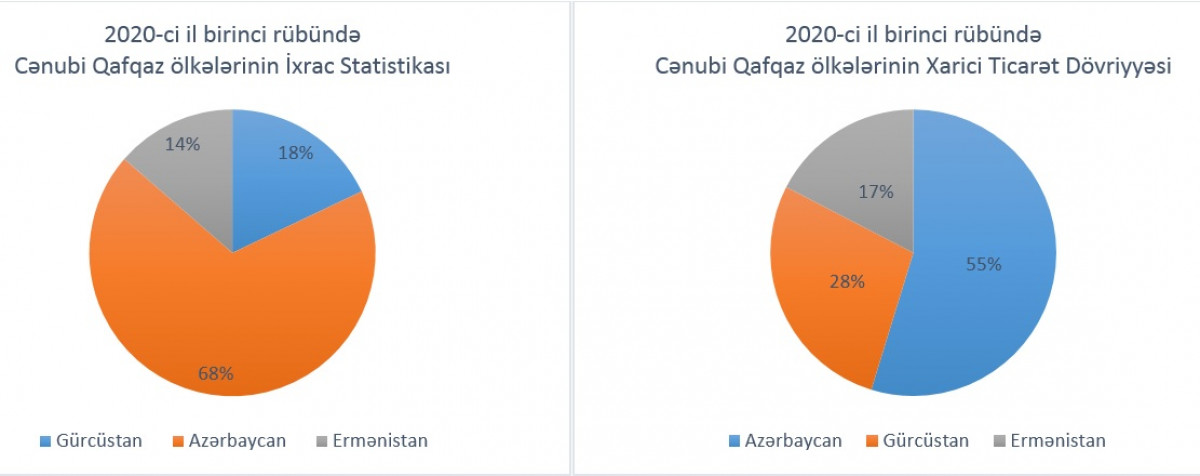

According to statistics for the first quarter of 2020, Armenia’s share in total exports of the South Caucasus is only 14 percent, the lowest in the region. For comparison, in 2019 the value of exports carried out by Armenia was 7.5 times lower than Azerbaijan’s exports. Armenia’s low export performance is the result of its exclusion from key transport and logistics opportunities due to conflicts with neighboring countries.

As a consequence of territorial claims against Azerbaijan, Armenia has been left outside major international projects implemented by Turkey and Azerbaijan in the region, which has kept its economic growth and development potential consistently low. In this context, if Armenia were to abandon its policy of territorial claims, it would be possible to restore economic activity in the country.

Import Dependence in a Consumption-Oriented Economy

An analysis of import growth rates suggests that, compared to exports, the negative balance of trade is likely to widen further in the coming years. Armenia recorded import growth of 20–25 percent during 2017–2019. Dependence on imported components for domestically produced goods, weak development of the processed food industry, the weak position of local production in the domestic market, and the limited number of sectors with comparative advantages provide a solid basis for increased demand for imported goods.

Armenia’s accession to the Eurasian Customs Union in 2015 further increased exports from other member states to Armenia. Weak domestic production under the “Made in Armenia” label encouraged consumers to prefer higher-quality products from Russia, Belarus, and Kazakhstan. In addition, the absence of a competitive manufacturing industry capable of competing with imported goods is linked to lagging quality standards. Within the Union, the reduction and elimination of import duties among member states under a unified customs tariff policy has given these countries a price advantage in Armenia’s domestic market. Furthermore, following Armenia’s accession to the European Union’s Generalised System of Preferences (GSP+), export operations from EU countries have also accelerated.

Nevertheless, under conditions of weak domestic production, Armenia’s ability to benefit from the privileges of the Eurasian Customs Union and the GSP+ program remains limited. Within the framework of these preferential systems, there has been no diversification of Armenia’s exports; on the contrary, imports have increased further, undermining the competitiveness of local producers.

There is a positive correlation between the decline in retail trade turnover over the first eight months of 2020, according to the Statistical Committee, and the decline in imports. Although the commodity structure of retail trade turnover is not widely diversified, the vast majority of goods are import-oriented. This reflects the fact that aggregate demand in Armenia is largely met through imports. In particular, since most items in the daily consumer basket—such as gasoline, food products, and pharmaceuticals—are import-dependent, any expected exchange rate volatility could lead to serious social discontent.

The main products dominating imports include petroleum products and gas, poultry meat, various agricultural products, tobacco, medical supplies, information technology equipment, and technological goods. By commodity structure, these goods constitute the daily and monthly consumption of households and legal entities. According to the Armenian Statistical Committee, retail trade turnover in 2019 amounted to USD 3.3 billion, with the largest share generated by shops (including supermarkets) at 76.7 percent (annual growth of 11.7%) and other trade outlets at 15.1 percent. Considering that imported products are predominantly sold through shops and taking into account the aforementioned positive correlation, it can be concluded that a large portion of the USD 2.5 billion turnover serves imports.

Declining Investment Income

Repatriation of investment income in the primary income balance has increased, forming a deficit of nearly USD 700 million. Due to the economic recession caused by the COVID-19 pandemic and the decline in foreign trade operations, the current account deficit over two quarters of 2020 decreased from USD 218 million to USD 143.6 million. Analysis shows that this reduction was not driven by growth in exports of goods and services or higher investment income, but rather by a 14 percent economic recession, a 13 percent decline in foreign trade turnover, and an 8.4 percent decrease in income from direct investments.

Given the high share of the mining sector in tax revenues, foreign currency inflows, and economic activity, contraction of this sector under pandemic and wartime conditions is inevitable. Moreover, according to a September 30 statement by the Central Bank of Armenia, foreign currency inflows from export operations are expected to decline by 12–15 percent by the end of 2020, while currency outflows through imports are projected to decrease by 15–17 percent.

Financial Account Balance

Under conditions of a balance of payments deficit, Armenia’s external debt is expected to increase further. At the same time, a depletion of foreign exchange reserves, a decline in the capital account, and growing dependence on external borrowing are anticipated. Armenia’s provocations against Azerbaijan, the low credit ratings of Armenian banks, and, most importantly, the deterioration of socio-political stability reduce the country’s confidence index and tighten the terms of external borrowing.

As of August 2020, Armenia’s foreign exchange reserves amounted to USD 2.6 billion (with no gold reserves), which is sufficient to cover approximately three months of imports. It should be noted that only part of the Central Bank’s reserves is liquid, and the premature sale of medium- and long-term assets in emergency situations could result in financial losses.

According to the structure of the balance of payments, indicators in the financial account do not differ from the unsustainable figures observed in the current account. An unfavorable business environment and monopolization make foreign investors cautious. According to data for the first half of 2020, foreign direct investment in the Armenian economy decreased by 115.8 percent compared to the same period in 2018 and by nine times compared to the same period in 2019. Portfolio investments have also declined in Armenia, where participation in international capital markets is limited. This is most likely due to the withdrawal of Russian non-resident investors from companies of strategic importance.

After leaving the Soviet Union, Armenia failed to fully realize its transition to a market economy due to the shadow economy. In such conditions, projected economic growth figures are clearly not reflected in real life. Moreover, due to conflicts with neighboring countries, Armenia relies solely on a northern route to access high-value markets, and high transportation costs undermine its competitiveness. The country attempts to ease social tensions among households and sustain the banking sector through remittances, but under escalating conflict it must be prepared for new scenarios.

In times of conflict, the first to be affected are non-residents and their capital, accelerating financial and capital repatriation. International experience shows that when confidence in the future weakens, property rights are violated, the right to peaceful living is undermined, governments tend toward poor governance, and, most critically, drag countries into war, both portfolio and direct investments leave the country. This leads to rising unemployment and poverty among the local population.

Conclusion

Armenia’s problem of “twin deficits”—the balance of payments deficit and the consolidated budget deficit—has placed the country face to face with the risks of new borrowing, further restrictions on political independence, and the loss of economic leverage. By remaining outside regional projects, Armenia has reached a dead end, and its provocations against its far stronger neighbor Azerbaijan on September 27 have accelerated this collapse. It is irrational for Armenia, which has failed to ensure its political and economic independence, to continue occupying 20 percent of Azerbaijani territories and pursuing a policy of economic militarism.

Related news

A round table discussion on the topic "Digital Architecture: Program Management…

In accordance with the strategic priorities set at the first meeting of the Digital Development Council of the Republic of Azerbaijan, chaired by Mehriban Aliyeva, First Vice-President of the Republic of Azerbaijan, a round table…

CAERC Representative Participates in an International Seminar on Agriculture in…

Rashad Najafli, Deputy Head of the Economic Analysis Division at the Center for Analysis of Economic Reforms and Communication, is participating in an international seminar titled "Quality and Safety Management of Agricultural…

IV Shusha Global Media Forum: A New Stage in the Institutional Development of Strategic…

The 4th Shusha Global Media Forum once again demonstrates that strategic communication has become an integral component of state governance in the modern global information environment. In a comment to AZERTAC, Zanura Talibova, Head…

Vusal Gasimli chaired a session at an international event held at the University…

Vusal Gasimli, Executive Director of the Center for Analysis of Economic Reforms and Communication, Doctor of Economic Sciences, Professor, chaired the "Finance and Growth" session at "The International Finance and…

Preliminary figures for the July 2026 issue of the "Export Overview" have…

The Center for Analysis of Economic Reforms and Communication (CAERC) has presented the July 2026 issue of the "Export Overview." According to the overview, in January-June 2026, Azerbaijan's exports in the non-oil sector…

CAERC Department Head’s Analytical Article Published by The Liberum

An analytical article authored by Ilyas Huseynov, Head of the Turkic World Research Center at the Center for Analysis of Economic Reforms and Communication (CAERC), has been published on the international analytical platform…

CAERC Representative Participates in International Seminar in China

A representative of the Center for Analysis of Economic Reforms and Communication (CAERC) participated in the international seminar "Governance Capacity Building for BRI Countries", held in the People's Republic of China.…

A meeting was held between "Azexport" and "Payoneer" regarding…

A business meeting was held between the "Azexport" portal, operated by the Center for Analysis of Economic Reforms and Communication (CAERC), and "Payoneer," an international digital payment system. The main topic…

Op-eds

Abdulrahim Dadashov

Deputy head of the Monitoring and evaluation division

Agricultural support mechanisms will create new opportunities for farmers and exporters

Ilyas Huseynov

Head of the Turkic World Research Center

Large-Scale Modernization of the Baku-Tbilisi-Kars Railway: A New Strategic Phase in the Middle Corridor and Eurasian Connectivity

Rashad Najafli

Deputy head of the Economic analysis division

Azerbaijan: A Guarantor of Peace and Security in the South Caucasus

Isa Gasimov

Head of the “Enterprise Azerbaijan” portal

Transition to an Innovation Ecosystem: Azerbaijan’s Strategic Choice

Gultaj Ahmadzada-Tapdigzada

Head of Sector at the Monitoring and Evaluation Division

Strategic Targets of Azerbaijan’s Energy Transformation

Samir Rahimov

Leading consultant of the Monitoring and evaluation division

Improving transport infrastructure in Baku and surrounding areas - Global challenges and the role of the State Program

Agil Asadov

Head of the Strategic planning division

The strategic importance of the Middle Corridor: growth of investment along the Trans-Caspian route and Azerbaijan’s regional…